Self-directed IRAs are one of the most underused startup fundraising tools available today, and for women founders navigating a system that's been stacked against them, that gap represents a real opportunity.

The numbers haven't moved in a decade. Funding for all-female founding teams has stayed stubbornly stuck in the low single digits as a share of total VC dollars.

The good news is that self-directed IRAs are one of the most underused startup fundraising tools available today.

Not because women aren't building, between 2019 and 2023, women-owned firms outpaced the broader market in revenue, firm count, and employment. And not because the companies aren't scaling, there are now 270,000+ women-owned employer firms generating over $1M in annual revenue.

The pipeline isn't the problem, the gatekeepers are.

Harvard Business Review documented what most women founders already feel in their bones: network-driven deal sourcing, pattern-matching bias, pitch evaluation processes that aren't neutral by design. The structural dynamics are well-documented at this point. What's less talked about is the large pool of capital that bypasses those gatekeepers entirely.

Why Women Founders Are Turning to Self-Directed IRAs

The broader VC environment isn't helping either. New VC investments hit their lowest annual total since 2018 in 2024, and the number of new venture funds raised in the U.S. declined 46% year-over-year, down 68% from the 2021 peak.

The money that's still moving isn't spreading out, the top 30 funds captured 75% of all VC capital raised in 2024, with just nine funds securing nearly half of that.

Founders and investors from underrepresented backgrounds are among those most affected by this consolidation. Which means women founders are navigating a system that was already structurally biased against them, at a moment when that system is concentrating power even further upward.

So the question isn't how to pitch better inside a system that's tightening. The question is what sits outside it.

How Self-Directed IRA Investing Works for Startups

IRAs represent approximately 40% of all U.S. retirement assets; over $19 trillion in long-term, tax-advantaged capital that can legally be directed into private market investments, in other words, startups, venture funds, SPVs, and early-stage deals.

Most investors have no idea their retirement savings can work this way and most founders have never thought to offer it as a path.

Despite the trillions of dollars Americans hold in IRAs, the biggest barrier to adoption isn't lack of interest but lack of awareness and the perception that alternatives and private markets are too complex to navigate.

There's also a generational dimension that makes this particularly relevant for women founders right now. An estimated 50–70% of long-term wealth is expected to transfer to women over the coming decades, driven by inheritance, longer life expectancy, and rising financial decision-making authority.

Women are increasingly the primary holders and allocators of retirement savings, and research shows 63% of women cite growth and income potential as primary drivers when evaluating alternative investments. The alignment between who's building, who's investing, and where the capital is sitting is real. The ecosystem just hasn't connected the dots yet.

Why IRA Capital Is Better Aligned With How Companies Actually Get Built

The thing that makes retirement capital genuinely interesting for founders isn't just the size of the number, it's what that capital is designed to do.

Investing through a self-directed IRA aligns long-term investment horizons with saving for retirement, a dynamic sometimes called "duration matching." Unlike public market investments, early-stage companies often build most of their value over many years in the private market before any liquidity event occurs.

IRA investors aren't optimizing for a 12-month flip, they're thinking in decades, which is actually much more compatible with how company-building works than the pressure cycles that come with institutional VC.

Gains inside the IRA grow sheltered from annual taxes, which means if the company expands significantly, returns can compound inside the retirement account without the drag of yearly tax obligations. For investors who believe in what you're building, this structure can make the investment considerably more attractive than deploying liquid cash into the same deal.

This capital also reaches a different investor base, which for women founders specifically, is the whole point.

How to Find IRA Investors for Your Startup Round

Think about who your most aligned potential investors actually are. Former colleagues who've watched you build.

Operators in adjacent spaces who get the problem you're solving. Community members who've been following your work for years. The people who would back you without needing a warm intro to trust you, because they already do.

For a lot of them, the obstacle isn't belief, it's liquidity. Their capital isn't sitting in a brokerage account waiting to be deployed into your round. It's in a 401(k) or IRA they've been contributing to for a decade, an account they've never thought of as a vehicle for investing in companies they believe in.

That's not a fringe case. That's the situation for a huge portion of the operator class, people in their 30s and 40s who have been quietly building retirement wealth and who, with the right mechanism, would absolutely put some of it behind the founders they believe in.

Without a clear path, they stay on the sidelines. Not because they didn't want to invest. Because nobody handed them the door.

How Women Invest Raised 23% of Its Fund III Through IRA Capital

How Women Invest, a VC firm backing 100% women-founded teams, decided to build IRA capital into its fundraising strategy deliberately rather than treating it as an afterthought.

The result: $3.16M of its total raise came in as retirement capital, representing approximately 23% of its Fund III. For LPs who wanted to participate but didn't have liquid capital readily available, self-directed IRAs became the mechanism that made it possible.

Across Alto's platform, IRA-funded startup raises have grown 16% year-over-year, and 67% of 2025 investments came from repeat investors, a signal that when investors find founders they believe in and can access the deal through retirement funds, they keep coming back.

The infrastructure isn't nascent, it works, the only thing lagging is founder awareness.

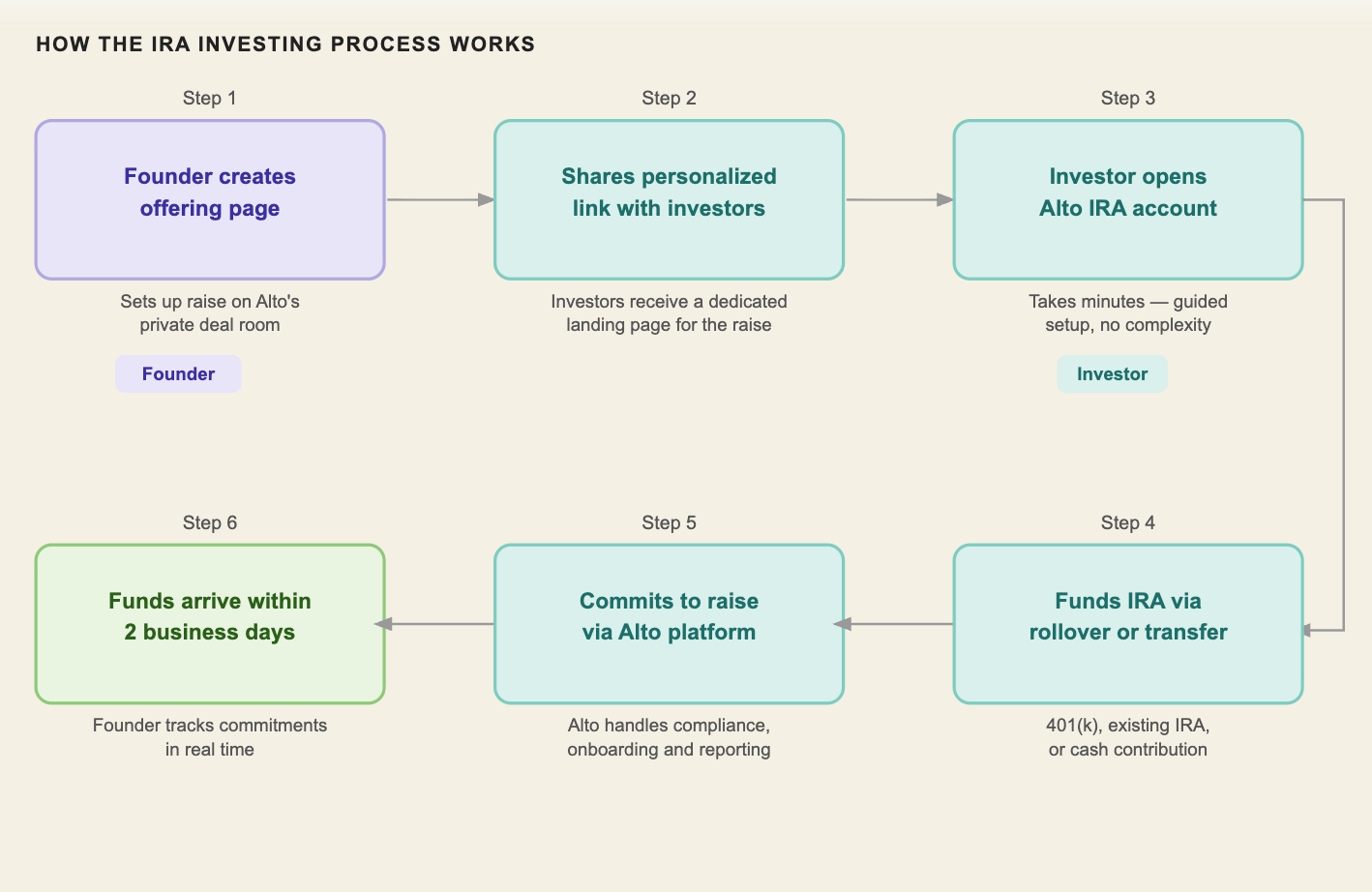

How to Start Raising IRA Capital With Alto

Alto acts as the custodian for self-directed IRAs, handling the account administration, compliance, investor onboarding, and ongoing support that makes IRA investing in private deals actually possible at scale.

Account fees are charged directly to investors as their investments are placed, meaning there is no placement fee and no cut of the raise for issuers. Every dollar you raise through IRA capital is yours.

For founders and fund managers, Alto's private deal room gives you a direct path to self-directed IRA capital with no technical integration required and no changes to how you're already managing your raise.

You set up an offering page, share a personalized link with prospective investors, and track commitments in real time. On the investor side, they receive a dedicated landing page to access the raise and can fund through rollovers, transfers, or cash contributions, whichever works for their situation. Funds typically arrive within two business days of transfer completion.

The back-end complexity, compliance, onboarding, reporting, investor support, is handled by Alto, so you stay focused on closing the round rather than managing the mechanics of it.

If you're actively raising and want to open this channel, you can get started with Alto here.

How to Add IRA Capital to Your Fundraising Strategy (Step by Step)

This doesn't require reinventing your fundraising process, it requires adding a lane.

Mention it proactively.

When you're talking to prospective investors, especially operators, former colleagues, community members, don't wait for them to ask. Most won't know to ask so you need to bring it up and tell them their retirement savings can participate in the round. That single conversation can unlock commitments that would otherwise never happen.

Make it part of your materials.

Add a line to your deck or your investor FAQ noting that IRA-compatible investing is available. It signals that you've done the work and removes friction for investors who need to figure out the logistics.

Point them to a custodian.

Self-directed IRA custodians like Alto handle the compliance, investor onboarding, and operational mechanics so founders don't have to manage the back-end themselves. Funds typically arrive within two business days of transfer completion, and the process is operationally streamlined for both sides.

Ask the right question.

For investors who express interest but hesitate on liquidity, it's simple: do you have retirement savings that could be deployed instead? Most of them haven't thought about it. Most of them can.

Why the Next Generation of Founders Will Raise Differently

The founders who navigate the next decade well won't just be better at pitching. They'll be better at thinking about capital as a multi-channel strategy rather than a single funnel with VCs at the top.

VC is one channel. Angels are another. Strategic investors, community rounds, revenue-based financing, these are all levers that increasingly sophisticated founders are pulling in parallel. IRA capital is one more lever, and right now it's dramatically underutilized relative to its actual size.

For women founders in particular, this matters because the traditional channel has a documented structural bias problem that hasn't meaningfully improved in a decade. The point isn't to abandon VC as a path, it's to stop treating it as the only path, especially when there's $19 trillion sitting in accounts that don't require a warm intro, don't require pattern-matching favorably in a partner meeting, and don't require you to fit a mold that wasn't built for you.

FAQs: Self-Directed IRAs and Startup Investing, Explained

What exactly is a self-directed IRA?

A self-directed IRA (SDIRA) is a retirement account that works like a standard IRA in terms of tax advantages and contribution rules, but gives you the ability to invest in a much broader range of assets. While traditional, Roth, SEP, and other IRAs can all technically be "self-directed," most brokerages and custodians don't allow investments in alternative assets, assets that aren't publicly traded. A self-directed IRA gives you the control and flexibility to invest in assets you know and understand, including startups, private equity, real estate, and more.

Is it actually legal to invest IRA money into startups?

Yes. Alto ensures the process follows IRS and SEC guidelines, giving both founders and investors confidence that each raise is handled correctly. The mechanism has existed for decades, the issue has never been legality, it's been awareness and access.

What types of IRAs can be used?

You can open a Traditional, SEP, or Roth self-directed IRA. A Traditional IRA is tax-deferred, meaning contributions may be tax-deductible and earnings grow tax-deferred until withdrawal. A SEP IRA is designed for self-employed individuals or small business owners and comes with potentially higher contribution limits. A Roth IRA is funded with after-tax dollars, offering tax-free growth and. subject to IRS rules, tax-free withdrawals in retirement. For long-term startup investments, the Roth structure is often the most powerful because gains can compound entirely tax-free.

Can investors roll over an existing 401(k) into a self-directed IRA?

Yes, in many cases you can roll over a 401(k) into a self-directed IRA, especially if you've left the employer who sponsored the plan. Rolling over into an SDIRA allows you to maintain the tax-advantaged status of your retirement funds while gaining access to a broader range of investments. Alto also supports transfers from existing IRAs, 401(a), 403(b), 457, and TSP accounts.

How complicated is the process for investors?

Less than most people assume. With Alto, investors can set up and fund a self-directed IRA in minutes through a streamlined process that allows them to invest in startups without unnecessary complexity. Alto handles compliance, onboarding, rollovers, and reporting on the back end so neither the investor nor the founder has to manage the mechanics manually.

Does it cost founders anything to accept IRA capital?

There's no cost to issuers raising IRA capital through Alto. The platform doesn't charge a payment processing fee, placement fee, or commissions, so founders receive every IRA dollar they raise. Account fees are charged directly to investors as part of their account management.

How quickly do funds arrive once an investment is committed?

Once investments are committed, funds are typically delivered within two business days. For founders mid-raise, that's a timeline comparable to most standard wire transfers.

What's the minimum investment amount?

Investors can participate in startup raises through an Alto IRA with as little as $100, depending on the minimum investment of the offering. The average check size in the private deal room is around $80,000.

Are there restrictions on which startups can accept IRA capital?

The main IRS restrictions relate to "prohibited transactions," meaning the IRA owner can't invest in a business they already control or that involves certain family members. For most arm's-length startup investments, this isn't an issue. Founders should confirm their deal structure with a custodian before launching, but the vast majority of standard raises are eligible without any structural changes.

.png)

.png)